Pre-Closing Reverifications

Re-verify employment from income or deposits.

Real-time, payroll-connected (VOE) or bank-connected (DVOE) reverification reports.

GSE-ready reports to streamline closing requirements.

GSE-ready reports to streamline closing requirements.

Data Quality

Unlock higher validation rates.

Leading rep & warrant relief acceptance rates with VOE and DVOE reports.

Learn more

Automation

Automate reverifications.

Trigger automated reverifications using ASO inside Encompass.

Learn more

Customization

Customize VOE and DVOE reports.

Stay clear to close with customized report data and on-demand refreshes.

Learn more

Cost Savings

Minimize exorbitant multi-report costs.

Save on verification costs with unlimited, free refresh reports for up to 90 days.

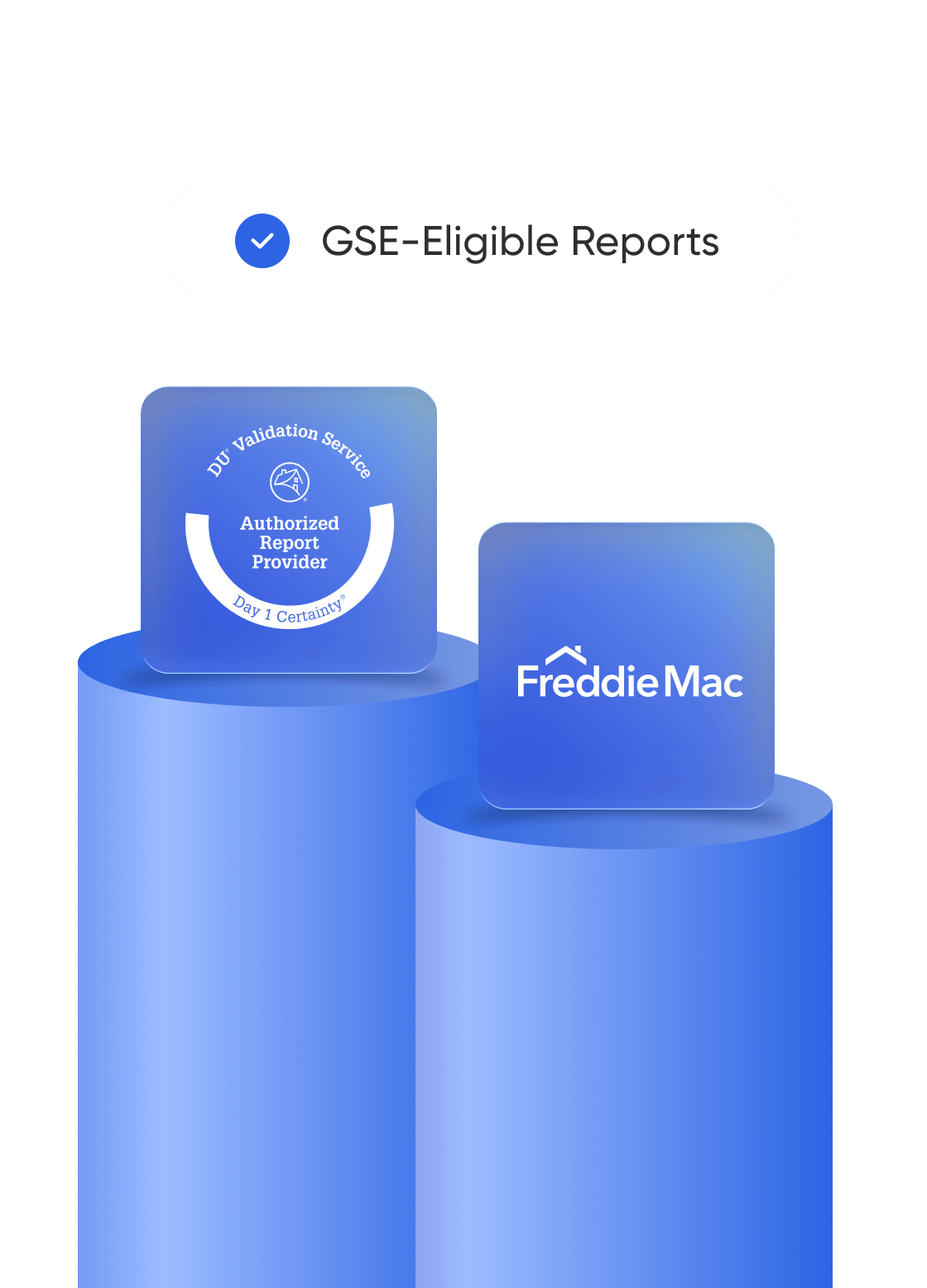

Learn more Increase validation rates with GSE-eligible reports.

Increase validation rates with GSE-eligible reports.

Day 1 Certainty®

Learn More

LPA AIM®

Learn More

Real results. Real Truv experiences.

Real results. Real Truv experiences.

Employment reverification FAQs.

Employment reverification FAQs.

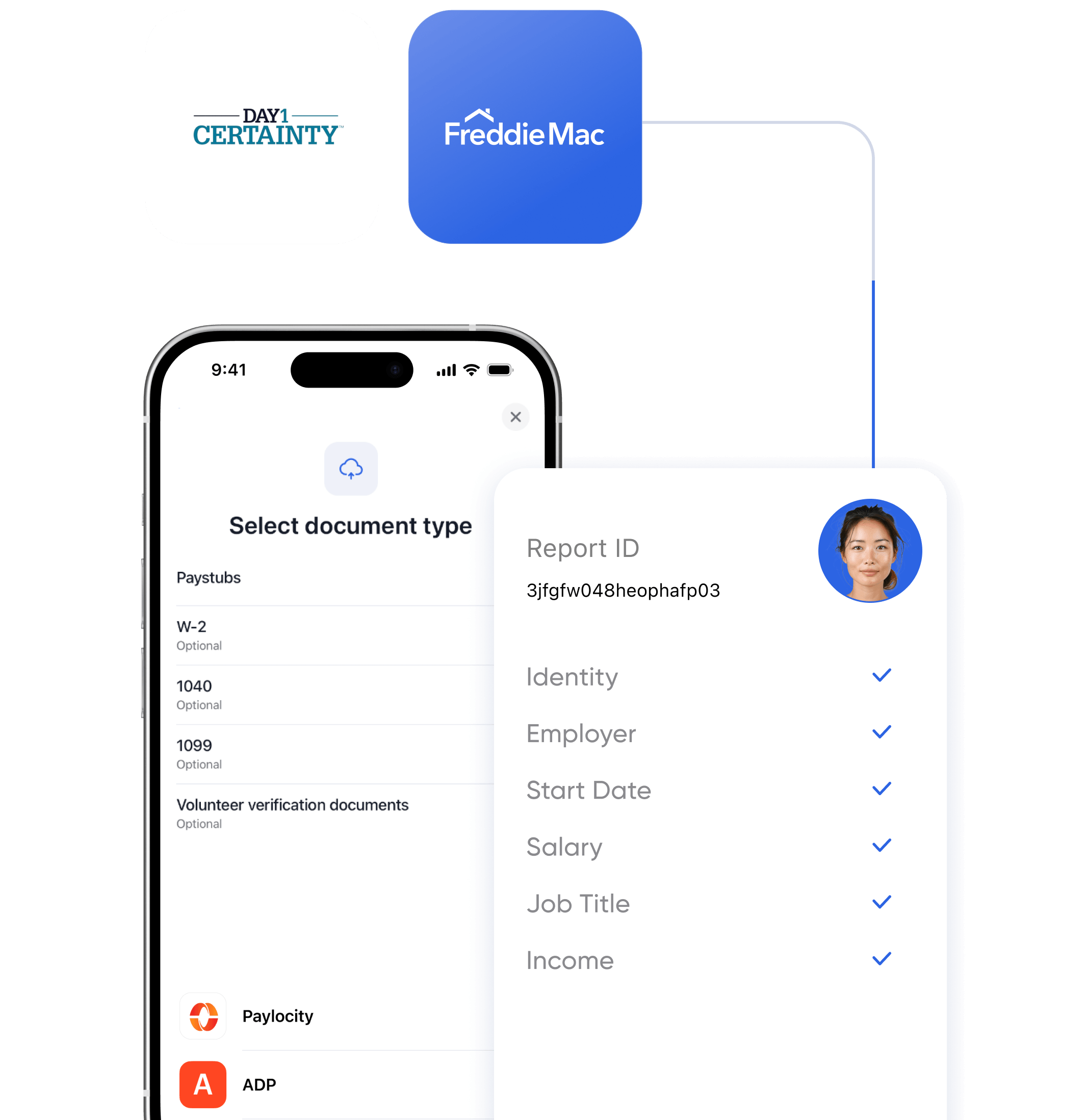

A pre-closing reverification is a refresh report mortgage lenders run roughly 10 days prior to closing to confirm a borrower is still employed and their income hasn’t significantly changed. Both Fannie Mae and Freddie Mac require a recent reverification before funding, and Truv supports this step with two compliance-ready report types: Verification of Employment (VOE) from payroll and Deposit-based Verification of Employment (DVOE) from bank assets.

Verification of Employment (VOE) is a report that confirms a borrower’s active employment status with their employer. When Truv’s Verification of Income and Employment is used upfront in the loan file, lenders can auto-generate a pre-closing VOE report 10 days before closing directly from their LOS or the Truv Dashboard. The report pulls real-time, payroll-connected data so underwriters and closers can clear-to-close faster.

Deposit-based Verification of Employment (DVOE) is a pre-closing report used when the borrower’s income was originally verified with Truv’s Verification of Assets earlier in the loan process. Truv generates the DVOE from connected bank account data, analyzing recent payroll deposits to confirm continued employment without requiring the borrower to reconnect or upload new documents.

Yes. Truv is an authorized report supplier for Fannie Mae’s Desktop Underwriter® (DU®) validation service (D1C®) and an approved provider for Freddie Mac’s Loan Product Advisor® (LPA℠) asset and income modeler (AIM®). Truv’s VOE and DVOE reports are designed to meet GSE pre-closing requirements and can support rep & warrant relief on eligible loans.

Lenders using ICE Mortgage Technology’s Encompass can trigger automated pre-closing reverifications through Truv’s Automated Service Order (ASO) integration. The reverification fires at the right point in the workflow, the report is delivered back into the loan file, and the closing team gets a refreshed VOE or DVOE without manually re-ordering — cutting cycle time.

A Verification of Employment (VOE) confirms employment using direct payroll-connected data and is the path Truv recommends when income was verified via payroll/employer connections initially. A Deposit-based Verification of Employment (DVOE) confirms employment using bank deposit data and is used when income was originally verified through Truv’s Verification of Assets. Both are GSE-eligible refresh reports — the right choice depends on how the borrower’s income was verified earlier in the loan.

Yes. Truv supports customizable VOE and DVOE reports so lenders can configure the data fields, refresh windows, and report types — including payroll-based VOE and deposit-based VOE — that match their underwriting and investor requirements. On-demand refreshes are available so lenders can stay clear-to-close even if the closing date moves.

Truv minimizes multi-report fees by including unlimited, free refresh reports for up to 90 days on the original verification. That means a single upfront VOIE or VOA can power both initial underwriting and the 10-day pre-closing reverification — without a second invoice — helping lenders meaningfully lower their per-loan verification spend.