Income verification helps landlords and financial institutions determine whether you meet their approval criteria. If you apply for a mortgage or a loan, the verification process reassures the lender about your ability to repay the loan. Landlords use verification to determine whether you earn enough money to afford your monthly rent.

Learn more about income verification, how it works and how it can benefit you if you’re looking for a rental or trying to get approved for a loan.

What Is Income Verification?

Income verification determines whether an individual is eligible for a loan, rental agreement or specific service. Verification helps the lender confirm your income source and calculate how much you earn.

The main purpose of performing income verification is to make sure you can afford to pay rent or make loan payments. Companies also use income verification as a form of risk management, since verifying your income reduces the risk that you’ll default on your payment obligations.

Here are a few income verification examples to explain why companies use this process:

- Mortgages: A mortgage is a major commitment. Income verification helps lenders determine whether you can afford monthly mortgage payments.

- Personal loans: Personal loan payments are typically lower than mortgage payments, but financial institutions still need to manage risk effectively. Income verification helps show bankers and consumer lenders you can afford to repay a personal loan over time.

- Job applications: Some employers use income verification when negotiating salaries. For example, if a candidate claims to make $100,000 per year at their current job, an employer may verify this claim before extending an offer.

How Do Companies Verify Income?

Traditional income verification involves providing pay stubs, W-2s, tax returns and other documents to a lender, landlord or prospective employer. Pay stubs contain your current wages, the total amount earned during the calendar year and how much your employer deducts for taxes and benefits.

W-2s show your employer’s name and employer identification number (EIN), your gross wages for the year and the total tax paid to federal, state and local taxing authorities. Tax returns include your gross income, adjusted gross income (AGI), taxable income, deductions and total tax paid during the year.

All three documents help companies determine whether you can afford to make monthly payments. If you’re trying to land a new job, these documents can help prospective employers craft attractive offers.

Tools and Technologies Used for Income Verification

With standard verification, you send copies of your personal documents to each company that requests them. This makes the traditional verification process more time-consuming, cumbersome, and higher friction. Fortunately, technology has made it possible for lenders, landlords and employers to use digital verification tools.

Some companies use databases to find information about applicants, while others use a process known as consumer-permissioned verification. Instead of handing over your personal information, you can use a consumer-permissioned income verification service.

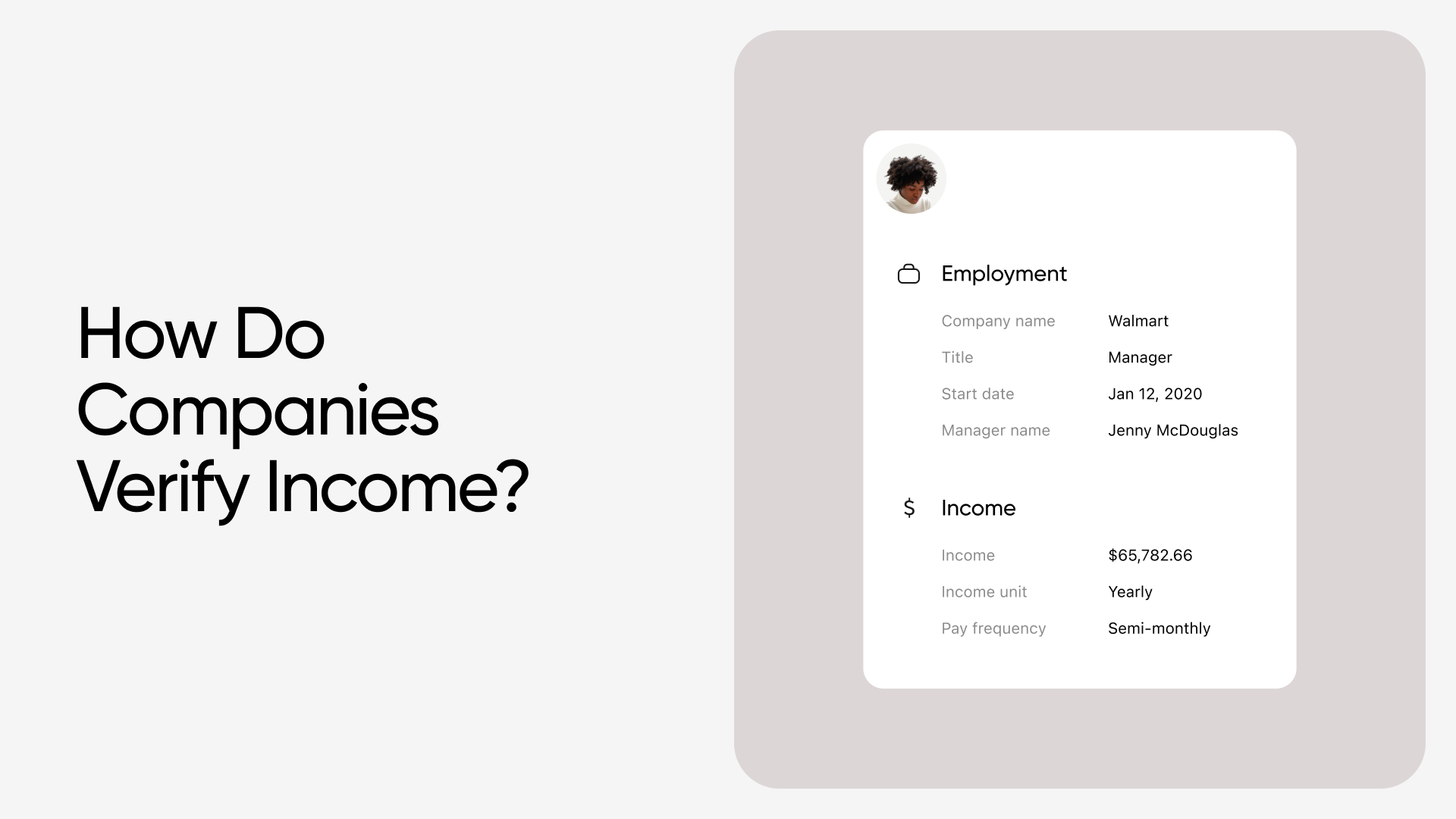

Consumer-permissioned data is information you share via a secure, encrypted platform. With Truv, you are prompted to select your employer or payroll provider, use your username and password credentials to login, and your verification is complete. Truv’s platform securely retrieves the information directly from the payroll provider and returns it to your lender, landlord, or bank. Consumer-permissioned data reduces the risk of fraud, as it allows companies to connect directly to your employer or payroll provider, eliminating copies of personal documents.

Since it relies on information provided by payroll providers, consumer-permissioned verification provides the most up-to-date information to the requesting party, in real-time.

The Role of Employment Verification in Income Verification

Many companies perform employment verification and income verification at the same time. Although these processes are closely linked, they have key differences.

Income verification helps banks and other companies determine your earnings. In contrast, employment verification helps verify your employment status and income stability, meaning you earn a consistent amount over time.

Companies verify your employment by contacting employers or using third-party verification services. Using a third-party service, like Truv’s consumer-permissioned verification platform, is more efficient than relying on manual verification.

Challenges in Income Verification and How Companies Address Them

Fraudulent documents and incomplete information are common challenges in income verification. Some borrowers submit fake pay stubs or other fraudulent documents to boost their chances of approval. Others forget to provide requested information, delaying the approval process.

Companies typically overcome these challenges by using secure methods of verification. For example, consumer-permissioned verification is more secure than manual verification, as companies can get the information they need from employers and payroll providers. This eliminates concerns regarding fraudulent documents.

These steps, along with industry-standard security measures, make it possible to perform accurate income verification.

Benefits of Proper Income Verification for Consumers

Consumer-permissioned income verification offers significant advantages, simplifying the process and improving the overall experience for applicants. Key benefits include:

- Faster review times: Digital verification tools significantly reduce the time it takes for lenders, landlords, or employers to evaluate your information, helping you move through the process more quickly.

- Less documentation required: Traditional verification often requires a pile of pay stubs, tax returns, or letters from employers. Consumer-permissioned tools streamline this by directly accessing the necessary data, saving you the hassle of gathering documents.

- No more paper chasing: Forget about searching for old forms or submitting multiple copies of the same document. Digital platforms connect directly to payroll providers or banks, eliminating the need for physical paperwork.

- Fewer follow-ups and delays: With accurate and secure access to your income data, there’s less back-and-forth communication, cutting down on frustrating delays or requests for missing information.

- Quicker approvals for loans or applications: By simplifying and speeding up the verification process, consumer-permissioned income verification helps you get decisions faster, whether you’re applying for a mortgage, personal loan, or rental property.

FAQs

The answers to the following frequently asked questions can give more insight into income verification.

How do they verify income?

Some companies verify income using pay stubs, tax returns and other documents. Others use consumer-permissioned verification, which makes the process more efficient.

How do you verify an income statement?

If you’re self-employed, you may have to provide an income statement to your lender or prospective landlord. Companies verify income statements by reviewing bank records and other documents. These documents can help verify the income listed on your provided statement.

How do you verify you have no income?

If you have no income, you may be able to submit a letter from Medicaid or another income-based government program. You might also provide a letter from your most recent employer indicating you’ve been laid off.